There are some comparatively convincing arguments for why fossil fuel divestment can’t do much to limit the severity of climate change, at least in terms of the direct effects from institutions selling their shares.

One important one is that people buying and selling stocks, and the changing value of the stocks, doesn’t directly profit or harm the company involved. A secondary market in shares is necessary to make IPOs possible, but once a company has gone public, it raises the money for big new fossil fuel projects in other ways, such as borrowing from banks.

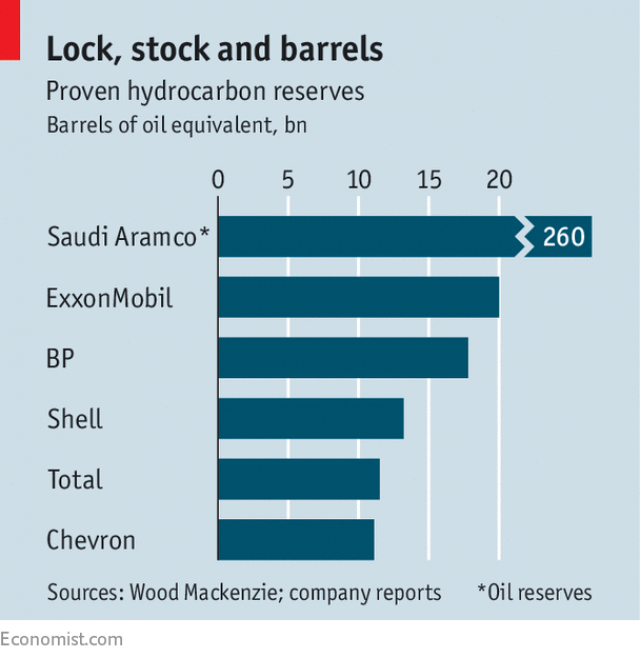

Another is that — while the proven reserves owned by companies like ExxonMobil are vast and can do considerable climate damage — sovereign countries have much larger reserves:

There are responses to these objectives, mainly in terms of how divestment is meant to gradually shift investor sentiment. Divestment is based on a financial as well as a moral case: if we really are going to control climate change, we can’t burn most of the world’s remaining coal, oil, and gas. As such, it makes no sense to develop big new projects, since we can’t even use all the resources in projects that have already been built. If it helps to spread that idea, divestment will have been worthwhile.

It might even help reduce the value of Saudi Aramco itself and the magnitude of its future investments, given that the firm is expected to be partly privatized in the near future.

There is symbolic imporatnce in a decision to divest for ethical reasons which has value.

THE proposal to sell shares in Saudi Aramco, the world’s biggest oil company, stunned the financial markets last year. Muhammad bin Salman, now Saudi Arabia’s crown prince, promised that it would be the biggest initial public offering (IPO) of all time, valuing Aramco at $2trn. It was to be the centrepiece of his plan to transform the Saudi economy, reducing its dependence on oil. It was meant to foster financial transparency and accountability in one of the world’s most hermetic kingdoms. Above all, it would cement the young prince’s image as a bold moderniser soon to inherit the throne.

…

The confusion is uncomfortable for Aramco, which, as national oil companies go, should be an attractive bet for investors. It has 15 times more reserves of oil and gas than ExxonMobil, its biggest private competitor, higher production, fewer employees and lower costs per barrel. It also has an abundance of young (including many female) engineers, and technology that can almost visualise the sea of oil beneath the desert sands. Its executives say that efficiencies inherited from the days that it was American-owned persist. Many Aramcons, as company officials are known, appear to view the IPO as an unwelcome distraction, but are at least mollified by the prestige they think an international listing would confer.

ExxonMobil said it would begin publishing estimates of the effects to its business from climate change and policies meant to fight it, a big win for the more than 60% of shareholders who passed a motion in May asking the company to disclose the risks it faces from global warming. Exxon had resisted the move for years.

In recent research we have completed at the University of Oxford’s Smith School of Enterprise and the Environment, we find that the direct impacts of fossil fuel divestment on equity or debt are likely to be limited. The maximum possible capital that might be divested by university endowments and public pension funds from the fossil fuel companies represents a relatively small pool of funds. Even if the maximum possible capital was divested from fossil fuel companies, their shares prices are unlikely to suffer precipitous declines.

But even if the direct impacts of divestment outflows are meagre in the short term, our research shows that a campaign can create long-term impact on the value of target firms through a process of stigmatisation. The outcome of this stigmatisation process, which the fossil fuel divestment campaign has triggered, poses a far-reaching threat to fossil fuel companies and the vast energy value chain. Any direct impacts of divestment pale in comparison.