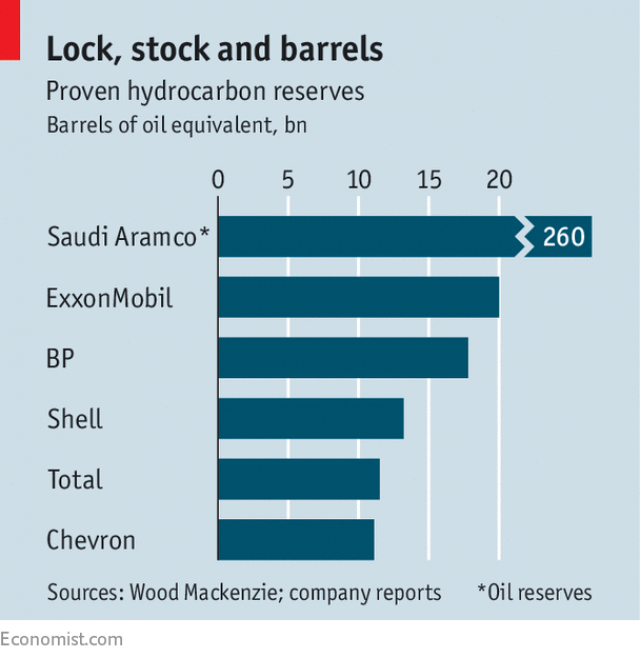

One of the most important economic and political points arising from climate change is uncertainty about how seriously future governments will respond to the problem. If some kind of political change makes governments serious about hitting the 1.5 – 2.0 ˚C temperature targets from the Paris Agreement, it will mean doing everything possible to rapidly reduce emissions, from imposing high carbon prices to mandating the abandonment of especially harmful technologies and practices like burning coal and using exceptionally filthy fuel for international maritime shipping. This is termed “regulatory risk”. Whenever a potential investment project has finances that rely on governments continuing to talk big but do little about climate change, the project risks becoming non-viable after all the costs of development are spent if the government subsequently starts to take climate change seriously.

When it comes to actual fossil fuel reserves, there is a related issue of “stranded assets” – fossil fuel reserves that would be economically viable to extract if they could be sold, but where the climate change and energy policies of governments either directly prohibit their extraction or add other costs like carbon taxes which make the extraction unprofitable. In such a scenario, firms that depended on the value of these reserves to justify their own market value could be in trouble, along with everyone who has invested in them.

A recent article in The Globe and Mail describes how firms are aware of these risks:

[Caisse de dépôt et placement du Québec] The Quebec-based pension fund is part of a growing tide of institutional investors – which includes giants such as Vanguard and BlackRock Inc. – pressing companies for more information on how they will manage the transition to a low-carbon economy. Companies in carbon-heavy industries such as energy and mining face the highest pressure, as investors fear being stuck holding stranded assets: companies who fail to plan for the future and whose valuations will likely plummet as a result.

“It’s a risk that we could be left holding the bag in a Minsky Moment and it could be quite costly,” says Toby Heaps, chief executive and co-founder of Corporate Knights Inc., a Toronto-based organization focused on corporate social responsibility. “I wouldn’t say we need to sound the fire alarm, but certainly it’s time to pause and take a serious look at how we can accelerate our transition to a low-carbon economy.”

The pressure has catapulted climate risk to the top of the agenda in many of Canada’s boardrooms as companies grapple with how to measure, mitigate and disclose potential liabilities. Last year, the board at Suncor Energy Inc. recommended that shareholders approve a proposal put forward by NEI Investments to enhance the company’s climate-related disclosures. Shareholders voted overwhelmingly in favour of the resolution.

There is every reason for advocates of stronger climate change mitigation policies to pressure firms to consider these risks before investing. There are ample examples of how – once a project is built and operating – it becomes politically impossible to shut down, regardless of how much harm it is causing. A classic example is coal-fired power plants in the United States that were built before the Clean Air Act and are thus exempt from the obligation to install scrubbers. Arguably, the entire bitumen sands is a massive example of a terrible idea that has become impossible to discontinue because too much has been invested, too many jobs are now at stake, and governments have become too dependent on royalties and other related revenue.